Sign in

Sign in

Profile

Profile Signout

Signout

CBSE Class 12 Pre-Board Exam 2024-25: Accountancy Most Important Questions with Answers – Free PDF Download

SHARING IS CARING

If our Website helped you a little, then kindly spread our voice using Social Networks. Spread our word to your readers, friends, teachers, students & all those close ones who deserve to know what you know now.

The CBSE Class 12 pre-board exams for 2024-25 are an important step in your exam preparation. These exams help you check how well you’re prepared for the final board exams.

To help you study better, we’ve created a list of the most important Accountancy questions with answers. This Accountancy question focuses on essential topics to help you perform well.

The CBSE Pre-board Exam Accountancy questions cover key topics. They include objective, short/long answer, and competency-based questions, all matching the latest exam pattern.

👉 Read Also - CBSE Class 12 Pre-Board Exam 2024-25: Chemistry Important Questions with Answers – Free PDF Download

👉 Read Also - CBSE Class 12 Pre-Board Exam 2024-25: Biology Important Questions with Answers – Free PDF Download

👉 Read Also - CBSE Class 12 Pre-Board Exam 2024-25: Physics Most Important Questions with Answers – Free PDF Download

👉 Read Also - CBSE Class 12 Pre-Board Exam 2024-25: Mathematics Most Important Questions with Answers – Free PDF Download

CBSE 12 Pre-board Exam 2024-25 Accountancy Most Important Questions

1. (a) Atul, Beena and Sita were partners in a firm sharing profits and losses in the ratio of 8 : 7 : 5. Damini was admitted as a new partner for 1/5 th share in the profits which she acquired entirely from Atul. The new profit sharing ratio after Damini's admission will be:

(A) 7:7:5:1

(B) 4:7:5:4

(C) 8:7:5:4

(D) 7:5:8:4

Ans. (B) 4:7:5:4

OR

(b) Rushil and Abheer were partners in a firm sharing profits and losses in the ratio of 4 : 3. They admitted Sunil as a new partner for 3/7 th share in the profits of firm, which he acquired 2/7 th share from Rushil and 1/7 th share from Abheer. The new profit sharing ratio of Rushil, Abheer and Sunil will be :

(A) 4 : 3 : 3

(B) 2 : 1 : 3

(C) 2 : 2 : 3

(D) 4 : 3 : 1

Ans. (C) 2 : 2 : 3

2. Abhay, Boris and Chetan were partners in a firm sharing profits in the ratio of 5 : 3 : 2. Boris was guaranteed a profit of ₹ 95,000. Any deficiency on account of this was to be borne by Abhay and Chetan equally. The firm earned a profit of ₹ 2,00,000 for the year ended 31st March, 2023. The amount given by Abhay to Boris as guaranteed amount will be :

(A) ₹ 17,500

(B) ₹ 35,000

(C) ₹ 25,000

(D) ₹ 10,000

Ans. (A) ₹ 17,500

3. Aavya, Mitansh and Praveen were partners in a firm. On 31st March, 2023, the firm was dissolved. Creditors took over furniture of book value of ₹ 50,000 at ₹ 45,000 in part settlement of their amount of ₹ 60,000. The balance amount was paid to them through cheque. The amount paid through cheque will be :

(A) ₹ 10,000

(B) ₹ 50,000

(C) ₹ 45,000

(D) ₹ 15,000

Ans. (D) ₹ 15,000

4. Piyush, Rajesh and Avinash were partners in a firm sharing profits and losses equally. Shiva was admitted as a new partner for an equal share. Shiva brought his share of capital and premium for goodwill in cash. The premium for goodwill amount will be divided among :

(A) Old partners in old ratio

(B) New partners in new ratio

(C) New partners in sacrificing ratio

(D) Old partners in sacrificing ratio

Ans. (D) Old partners in sacrificing ratio

| Download PDF | |

| CBSE 12 Pre-board Exam 2024-25 Accountancy Most Important Questions | Click Here |

5. Alex, Benn and Cole were partners in a firm sharing profits and losses in the ratio of 5 : 3 : 2. They admitted Dona as a new partner for 1/5 th share in the future profits. Dona agreed to contribute proportionate capital. On the date of admission, capitals of Alex, Benn and Cole after all adjustments were ₹ 1,20,000; ₹ 80,000 and ₹ 1,00,000 respectively.

The amount of capital brought in by Dona will be :

(A) ₹ 75,000

(B) ₹ 60,000

(C) ₹ 65,000

(D) ₹ 70,000

Ans. (A) ₹ 75,000

6. Assertion (A) : Each partner is a principal as well as an agent for all the other partners.

Reason (R) : As per the definition of Partnership Act, partnership business may be carried on by all the partners or any of them acting for all.

Choose the correct option from the following :

(A) Both Assertion (A) and Reason (R) are correct, but Reason (R) is not the correct explanation of Assertion (A).

(B) Both Assertion (A) and Reason (R) are correct and Reason (R) is the correct explanation of Assertion (A).

(C) Assertion (A) is correct, but Reason (R) is incorrect.

(D) Assertion (A) is incorrect, but Reason (R) is correct.

Ans. (B) Both Assertion (A) and Reason (R) are correct and Reason (R) is the correct explanation of Assertion (A).

Read the following hypothetical situation and answer questions No. 7 and 8 on the basis of the given information.

Abha and Babita were partners in a clay toy making firm sharing profits in the ratio of 2 : 1. On 1st April, 2023, their capital accounts showed balances of ₹ 5,00,000 and ₹ 10,00,000 respectively. The partnership deed provides for interest on capital @ 10% p.a. The firm earned a profit of ₹ 90,000 during the year.

7. The amount of interest on capital allowed to Abha will be :

(A) ₹ 50,000

(B) ₹ 1,00,000

(C) ₹ 60,000

(D) ₹ 30,000

Ans. (D) ₹ 30,000

8. Babita's share in profit will be:

(A) ₹ 60,000

(B) ₹ 30,000

(C) Nil

(D) ₹ 1,00,000

Ans. (C) Nil

9. Alfa Ltd. invited applications for 50,000 equity shares of ₹ 10 each at a premium of 30%. The whole amount was payable on application. Applications were received for 2,50,000 shares. The company decided to allot the shares on a pro-rata basis to all the applicants. The amount refunded by the company was :

(A) ₹ 32,50,000

(B) ₹ 15,60,000

(C) ₹ 39,00,000

(D) ₹ 26,00,000

Ans. (D) ₹ 26,00,000

10. Reserve capital is that part of _________ capital which cannot be called except at the time of winding up of the company.

(A) Issued

(B) Called up

(C) Uncalled

(D) Nominal

Ans. (C) Uncalled

11. Xeno Ltd. issued 25,000 equity shares of ₹ 10 each. The amount was payable as follows :

On Application — ₹ 4 per share

On Allotment — ₹ 5 per share

On First and Final call — Balance

All the shares offered were applied for and allotted. All the money due on allotment was received except on 1,500 shares. These shares were forfeited immediately after allotment. First and final call was not yet made. At the time of forfeiture, Share Capital Account will be debited by :

(A) ₹ 15,000

(B) ₹ 24,000

(C) ₹ 13,500

(D) ₹ 18,000

Ans. (C) ₹ 13,500

12. Assertion (A) : Irredeemable debentures are also known as perpetual debentures.

Reason (R) : The company does not give any undertaking for the repayment of money borrowed by issuing such debentures. They are repayable on the winding up of the company or on the expiry of a long period.

Choose the correct option from the following :

(A) Both Assertion (A) and Reason (R) are correct and Reason (R) is the correct explanation of Assertion (A).

(B) Both Assertion (A) and Reason (R) are correct, but Reason (R) is not the correct explanation of Assertion (A).

(C) Assertion (A) is incorrect, but Reason (R) is correct.

(D) Assertion (A) is correct, but Reason (R) is incorrect.

Ans. (A) Both Assertion (A) and Reason (R) are correct and Reason (R) is the correct explanation of Assertion (A).

13. (a) Money received in advance from shareholders before it is actually called up by the directors is :

(A) debited to calls in advance account

(B) credited to calls in advance account

(C) debited to share capital account

(D) credited to share capital account

Ans. (B) credited to calls in advance account

OR

(b) An offer of securities or invitation to subscribe securities to a select group of persons is termed as :

(A) Buy back of shares

(B) Employee stock option plan

(C) Private placement of shares

(D) Sweat Equity

Ans. (C) Private placement of shares

14. (a) A share of ₹ 100 on which ₹ 80 is received is forfeited for non-payment of final call of ₹ 20. The minimum price at which this share can be reissued is :

(A) ₹ 120

(B) ₹ 100

(C) ₹ 80

(D) ₹ 20

Ans. (D) ₹ 20

OR

(b) Shiv Ltd. forfeited 500 shares of ₹ 10 each on which ₹ 7 per share was paid. These shares were reissued for ₹ 9 per share fully paid. Amount transferred to Capital Reserve Account will be :

(A) ₹ 3,000

(B) ₹ 5,000

(C) ₹ 4,500

(D) ₹ 3,500

Ans. (A) ₹ 3,000

15. (a) Dan, Elf and Furhan were partners in a firm sharing profits in the ratio of 5 : 3 : 2. With effect from 1st April, 2023, they decided to change their profit sharing ratio to 2 : 3 : 5. There existed a General Reserve of ₹ 90,000 on the date of change in profit sharing ratio. The partners decided not to distribute General Reserve.

The necessary adjustment entry to show the effect of the above will be :

Ans.

OR

(b) Sia, Tom and Vidhi were partners in a firm sharing profits in the ratio of 3 : 2 : 1. With effect from 1st April, 2023, they decided to share profits and losses in the future in the ratio of 1 : 2 : 3. There existed a Debit Balance of ₹ 60,000 in Profit and Loss Account on that date.

The necessary journal entry for distribution of the balance in the Profit and Loss Account will be :

Ans.

16. (a) Anju, Divya and Bobby were partners in a firm sharing profits and losses in the ratio of 3 : 2 : 1. Bobby retired. The new profit sharing ratio between Anju and Divya after Bobby's retirement was 5 : 3.

The gaining ratio of remaining partners will be :

(A) 3 : 2

(B) 5 : 3

(C) 3 : 1

(D) 2 : 3

Ans. (C) 3 : 1

OR

(b) Mita, Veena and Atul were partners in a firm sharing profits and losses in the ratio of 3 : 2 : 1. Atul retired and his share was taken over by Mita and Veena in the ratio of 1 : 4. The new profit sharing ratio between Mita and Veena after Atul's retirement will be:

(A) 3 : 2

(B) 8 : 7

(C) 7 : 3

(D) 2 : 3

Ans. (B) 8 : 7

17. Aamir, Bashir and Chirag were partners in a firm sharing profits and losses in the ratio of 3 : 3 : 2. Chirag retired. Aamir and Bashir decided to share profits and losses in future in the ratio of 1 : 2. On the day of Chirag's retirement, goodwill of the firm was valued at ₹ 5,40,000. Calculate gaining ratio and pass necessary journal entry to record the treatment of goodwill (without opening goodwill account) on Chirag's retirement.

Ans. Gain = New share – Old Share

Aamir’s Gain = 1/ 3 - 3/8 = -1/24 (sacrifice)

Bashir’s Gain = 2/3 - 3/8 = 7/24 (gain)

18. Pearl and Ruby were partners in a firm with a combined capital of ₹ 2,50,000. The normal rate of return was 10%. The profits of the last four years were as follows:

The closing stock for the year 2022 - 23 was overvalued by ₹ 5,000.

Calculate goodwill of the firm based on three years' purchase of the last four years' average super profit.

Ans. Calculation of Normal Adjusted Profit

19. (a) Sunrise Ltd. acquired assets of ₹ 3,60,000 and took over creditors of ₹ 1,00,000 from Moonlight Ltd. for an agreed purchase consideration of ₹ 4,80,000. Sunrise Ltd. issued 9% Debentures of ₹ 100 each at a discount of 4% in satisfaction of the purchase consideration.

Pass necessary journal entries in the books of Sunrise Ltd. Show your workings clearly.

Ans.

OR

(b) Grapple Ltd. took over assets of ₹ 25,00,000 and liabilities of ₹ 5,00,000 from Allore Ltd. for an agreed purchase consideration of ₹ 18,00,000. Grapple Ltd. issued 11% Debentures of ₹ 100 each at 20% premium in satisfaction of the purchase consideration.

Pass necessary journal entries in the books of Grapple Ltd. Show your workings clearly.

Ans. In the books of Grapple Ltd.

Working Note:

No. of debentures = (Purchase Consideration) / Issue Price

= 18,00,000 / 120

= 15,000

20. (a) Mohan, Suhaan and Adit were partners in a firm sharing profits and losses in the ratio of 3 : 2 : 1. Their fixed capitals were : ₹ 2,00,000, ₹ 1,00,000 and ₹ 1,00,000 respectively. For the year ended 31st March, 2023, interest on capital was credited to their accounts @ 8% p.a. instead of 5% p.a.

Pass necessary adjusting journal entry. Show your workings clearly.

Ans. Solution:

Working Notes:

(b) Manoj and Nitin were partners in a firm sharing profits and losses in the ratio of 2 : 1. On 31st March, 2023, the balances in their capital accounts after making adjustments for profits and drawings were ₹ 90,000 and ₹ 80,000 respectively. The net profit for the year ended 31st March, 2023 amounted to ₹ 30,000. During the year Manoj withdrew ₹ 40,000 and Nitin withdrew ₹ 20,000. Subsequently, it was noticed that Interest on Capital @ 10% p.a. was not provided to the partners. Also Interest on Drawings to Manoj ₹ 3,000 and to Nitin ₹ 2,000 was not charged.

Pass necessary adjusting journal entry. Show your workings clearly.

Ans.

Working Notes:

Calculation of Opening Capital

21. Shivalik Limited was registered with an authorized capital of ₹ 10,00,000 divided into equity shares of ₹ 10 each.

It offered 50,000 equity shares to the public. The amount was payable as follows :

On Application — ₹ 2 per share

On Allotment — ₹ 6 per share

On First and Final call — Balance

The issue was fully subscribed. All the amounts were duly received except the allotment and first and final call money on 4,000 equity shares. These equity shares were forfeited.

Present the Share Capital in the Balance Sheet of the company as per Schedule III, Part I of the Companies Act, 2013. Also prepare 'Notes to Accounts' for the same.

Ans.

Notes to Accounts:

22. Archana, Vandana and Arti were partners in a firm sharing profits and losses in the ratio of 5 : 3 : 2. Their Balance Sheet on 31st March, 2023 was as follows :

Balance Sheet of Archana, Vandana and Arti as at 31st March, 2023

The firm was dissolved on the above date.

(i) Assets were realised as follows :

Debtors — ₹ 40,000

Stock — ₹ 50,000

Plant — ₹ 60,000

(ii) 25% of the Investments were taken over by Vandana at ₹ 18,000. Remaining Investments were taken over by Archana at 10% less than its book value.

(iii) Expenses of realisation ₹ 20,000 were paid by Arti.

Prepare Realisation Account.

Ans.

23. Azhar, Sumit and Robit were partners in a firm sharing profits and losses in the ratio of 3 : 1 : 1. Their Balance Sheet as at 31st March, 2023, was as follows :

Balance Sheet of Azhar, Sumit and Robit as at 31st March, 2023

Robit died on 30th June, 2023. According to the Partnership deed, Robit's legal representatives were entitled to :

(i) Balance in his Capital Account.

(ii) His share of General Reserve.

(iii) Interest on capital @ 10% p.a.

(iv) His share of goodwill. Goodwill of the firm was valued on the basis of thrice the average of the past four years' profits.

(v) His share in profits up to the date of death on the basis of the profit for the last year.

Profit for the previous years were :

Prepare Robit's Capital Account to be rendered to his legal representatives.

Ans.

Working Notes:

(i) Goodwill = 3 x 56,000/4 = 42,000

Robit’s Share in firm’s Goodwill = 42,000 x 1/5 = 8,400

Gaining ratio between Azhar and Sumit = 3:1

(ii) Robit’s Share in the Profit upto the date of death = 15,000 x 1/5 x 3/12

= 750

24. On 1st April, 2022, Zubian Ltd. issued ₹ 10,00,000, 7% Debentures of ₹ 100 each at a premium of 6%, redeemable at a premium of 4% after five years. The company had a balance of ₹ 30,000 in Securities Premium Account.

(a) Pass necessary journal entries for issue of debentures and for writing off 'Loss on Issue of Debentures' utilising Securities Premium Account at the end of the first year itself.

Ans.

(b) Prepare 'Loss on Issue of Debentures Account' for the year ended 31st March, 2023.

Ans.

25. (a) Qumtan Ltd. invited applications for issuing 1,00,000 equity shares of ₹ 10 each at a premium of ₹ 6 per share. The amount was payable as follows :

On Application and Allotment — ₹ per share

(including premium ₹ 3)

On First and Final call — Balance (including premium)

Applications for 1,60,000 shares were received. Applications for 10,000 shares were rejected and pro-rata allotment was made to the remaining applicants. Excess money received on application and allotment was returned. Dheeraj, who was allotted 200 shares, failed to pay the first and final call money. His shares were forfeited. All the forfeited shares were reissued at ₹ 5 per share fully paid up.

Pass necessary journal entries in the books of Qumtan Ltd.

Ans.

OR

(b) Printkit Limited invited applications for issue of 80,000 equity shares of ₹ 10 each. The amount was payable as follows :

On Application — ₹ 3 per share

On Allotment — ₹ 2 per share

On First and Final call — Balance

Applications for 1,50,000 shares were received. Applications for 10,000 shares were rejected and pro-rata allotment was made to the remaining applicants on the following basis :

Category A — Applicants for 80,000 shares were allotted 40,000 shares.

Category B — Applicants for 60,000 shares were allotted 40,000 shares.

Excess money received on application was adjusted towards amount due on allotment and first and final call. All the amounts due on allotment and first and final call were duly received.

Pass necessary journal entries in the books of Printkit Limited.

Ans.

26. (a) Shubhi and Revanshi were partners in a firm sharing profits and losses in the ratio of 3 : 2. Their Balance Sheet as at 31st March, 2023 was as follows :

Balance Sheet of Shubhi and Revanshi as at 31st March, 2023

On 1st April, 2023 they admitted Pari into the partnership on the following terms :

(i) Pari will bring ₹ 50,000 as her capital and ₹ 50,000 for her share of premium for goodwill for 1/4 th share in the profits of the firm.

(ii) Fixed assets were depreciated @ 30%.

(iii) Stock was valued at < 45,000.

(iv) Bank loan was paid off.

(v) After all adjustments capitals of Shubhi and Revanshi were to be adjusted taking Pari's capital as the base. Actual cash was to be paid off or brought in by the old partners as the case may be.

Prepare Revaluation Account and Partners' Capital Accounts.

Ans.

OR

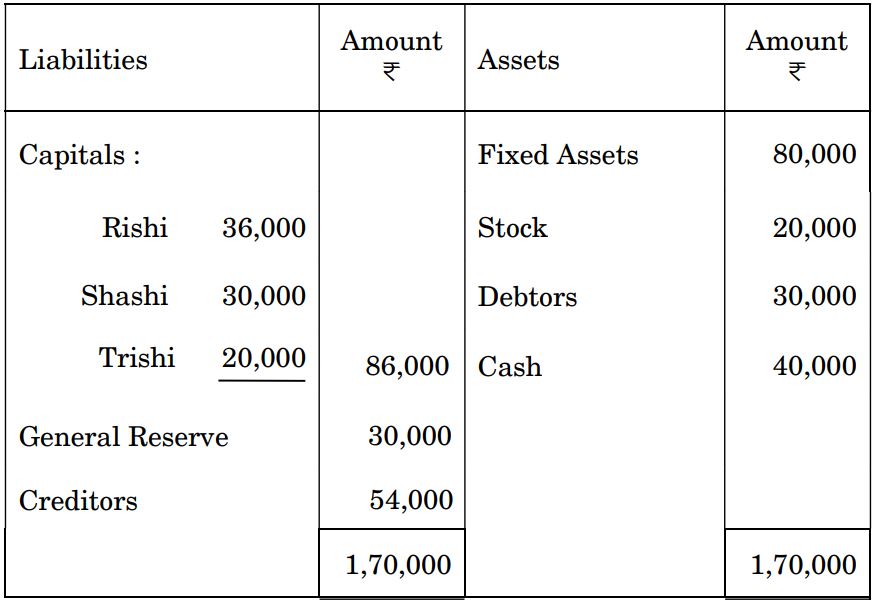

(b) Rishi, Shashi and Trishi were partners in a firm sharing profits and losses in proportion of 1/2, 1/6 and 1/3 respectively. Their Balance Sheet as at 31st March, 2023 was as follows :

Balance Sheet of Rishi, Shashi and Trishi as at 31st March, 2023

Shashi retired from the firm on 1st April, 2023 on the following terms :

(i) Fixed Assets were valued at ₹ 56,000.

(ii) Stock was taken over by Shashi at ₹ 26,000.

(iii) Goodwill of the firm was valued at ₹ 18,000 on Shashi's retirement

(iv) Balance in Shashi's Capital Account was transferred to her loan account.

Prepare Revaluation Account and Partners' Capital Accounts.

Ans.

27. The Quick Ratio of a company is 1 : 2. Which of the following transactions will result in an increase in this ratio ?

(A) Cash received from debtors

(B) Sold goods on credit

(C) Purchased goods on credit

(D) Purchased goods on cash

Ans. (B) Sold goods on credit

28. Identify which of the following transactions will result in 'Cash Inflow From Operating Activities':

(A) Payment to creditors

(B) Interest received by a non-finance company

(C) Dividend received by a non-finance company

(D) Amount received from debtors

Ans. (D) Amount received from debtors

29. (a) Analysis of Financial Statements is useful and significant to different users. Which of the following users is particularly interested in the firm's ability to meet their claims over a very short period of time?

(A) Labour Unions

(B) Trade Payables

(C) Top Management

(D) Finance Manager

Ans. (B) Trade Payables

OR

(b) ___________ ratios are calculated to determine the ability of the business to service its debt in the long run.

(A) Liquidity

(B) Turnover

(C) Solvency

(D) Profitability

Ans. (C) Solvency

30. (a) The transaction 'Acquisition of machinery by issue of equity shares of ₹ 5,00,00,000' will result in :

(A) Cash inflow of ₹ 5,00,00,000 from financing activities

(B) Cash outflow of ₹ 5,00,00,000 from financing activities

(C) Cash outflow of ₹ 5,00,00,000 from investing activities

(D) No flow of cash

Ans. (D) No flow of cash

OR

(b) The transaction 'Capital Gains Tax paid on sale of fixed assets' is classified under which of the following:

(A) Operating Activities

(B) Investing Activities

(C) Financing Activities

(D) Cash and Cash Equivalents

Ans. (B) Investing Activities

31. Classify the following items under major heads and sub-heads (if any) in the Balance Sheet of the company as per Schedule III Part I of the Companies Act, 2013 :

(a) Long Term Loans from Bank

(b) Loose Tools

(c) Outstanding Expenses

Ans.

| Item | Major Heads | Sub heads |

| (a) Long Term Loans from Bank | Non –Current Liabilities | Long Term Borrowings |

| (b) Loose Tools | Current Assets | Inventories |

| (c) Outstanding Expenses | Current Liabilities | Other Current Liabilities |

32. From the given information, calculate :

(a) Quick Ratio

(b) Inventory Turnover Ratio

| Particulars | Amount (₹) |

|

Current Assets Inventory Current Liabilities Net Profit Before Tax Revenue from Operations Gross Profit Ratio 20% |

4,00,000 1,00,000 2,00,000 7,20,000 10,00,000

|

Ans.

33. (a) From the given Balance Sheet of Geox Ltd., prepare Common Size Balance Sheet :

Ans.

OR

(b) From the following information, prepare a Comparative Statement of Profit and Loss for the year ended 31st March, 2022 and 2023 :

| Particulars | Note No. |

2022 - 23 (₹) |

2021 - 22 (₹) |

|

Revenue from operations Employee benefit expenses Other expenses Tax rate 50% |

10,00,000 2,50,000 5,50,000

|

8,00,000 1,00,000 4,00,000

|

Ans.

34. From the following information, calculate 'Cash Flows From Operating Activities':

| Particulars | Amount (₹) |

|

Surplus i.e. Balance in Statement of Profit and Loss Provision for Tax Proposed Dividend for the previous year Depreciation Loss on Sale of Machinery Gain on Sale of Investments Dividend Received on Investments Increase in Current Liabilities Increase in Current Assets (other than cash and cash equivalents) Decrease in Current Liabilities Income Tax Paid |

6,28,000 1,50,000 72,000 1,40,000 30,000 20,000 6,000 1,61,000 6,00,000 64,000 1,18,000 |

Ans.

-

👉 Read Also - CBSE Class 12 Half-Yearly/Mid Term 2024-25 : Most Important Questions with Answers; PDF Download (All Subjects)

👉 Read Also - How CBSE’s New Exam Pattern Will Impact Class 11 and 12 Students

Quiz

Quiz